-

Agentic AI and the Finance Enterprise: Automating B2B Receivables, Merchant Settlements, and Global Collections at Scale

Agentic AI and the Finance Enterprise: Automating B2B Receivables, Merchant Settlements, and Global Collections at Scale

Agentic AI for finance refers to autonomous multi-agent systems that ingest unstructured financial data e.g. bank statements, PSP settlement files, remittance emails etc. and match it using deterministic rules and AI reasoning, and orchestrate downstream actions (GL postings, dunning emails, exception cases) without human intervention for the majority of transactions. The result: higher straight-through processing (STP), reduced unapplied cash, and audit-ready governance at enterprise scale.

Posted by

AI Transformation Desk

Posted at

AI Transformation

Posted on

The Finance Automation Paradox

Most global enterprises have spent the past decade modernising their ERP systems, upgrading to cloud finance platforms, and investing in business intelligence. And yet, for the majority of organisations, a surprising truth remains: the majority of B2B cash application is still manual.

According to IOFM and Ardent Partners, 60 to 70 per cent of cash application processes still rely on manual intervention. The average time to identify an unknown payer is three to five days. The average annual cost of poor accounts receivable (AR) data quality exceeds $6.5 million for mid-size enterprises. And 23% of B2B invoices require some form of manual touch before they can be posted.

This is the finance automation paradox: organisations have invested heavily in back-office technology, but the intersection of B2B invoicing, multi-rail payments, and PSP settlement has remained stubbornly resistant to automation. The reason is structural.

The data that finance teams need to reconcile (remittance advice trapped in emails, PSP settlement files in proprietary formats, bank statements arriving via SWIFT and SEPA) does not fit neatly into the rule-based logic that drives traditional automation.

Robotic Process Automation (RPA) can automate keystrokes. Business Intelligence can visualise aging. But neither can read a scanned remittance PDF, infer the payment intent from an ambiguous bank reference, aggregate multiple invoices into a single payment, or autonomously route an exception to the right person with all supporting context pre-populated.

This is where Agentic AI changes everything.

Sources: McKinsey Global Institute, IOFM, Ardent Partners B2B Payments 2024

What Is Agentic AI? A Definition for Finance Leaders

Before examining how Agentic AI transforms finance operations, it is worth establishing a precise definition that separates genuine Agentic AI from the marketing noise that surrounds it.

Agentic AI refers to systems composed of multiple autonomous AI agents, each specialised for a specific task, that collaborate to complete complex, multi-step workflows without requiring continuous human instruction. Unlike single-model AI tools, Agentic AI systems can ingest diverse data sources, reason across context, take actions (such as posting to an ERP or sending a dunning email), and learn from feedback, all within a governance framework that ensures auditability and human oversight for exceptions.

In the context of enterprise finance, an Agentic AI system typically operates as an orchestration layer that sits between the chaos of external financial data (banks, payment service providers, partner portals) and the internal system of record (the ERP or general ledger). It does not replace the ERP. It provides the intelligence to bridge the two worlds.

The Hidden Complexity of Global B2B Finance Operations

Even organisations with mature ERP systems and capable finance teams face a structural bottleneck when operating at global scale. The problem is not competence; it is the nature of the data environment in which B2B finance operates.

The Three Recurring Operational Failures

1. The Matching Gap

Payments arrive via multiple rails (SWIFT, SEPA, Faster Payments, ACH) each with different reference formats and varying levels of data completeness. A SWIFT MT103 message may carry a structured reference; a SEPA credit transfer may carry none. Worse, the most critical payment information i.e. the specific invoice numbers being settled, partial payment allocations, or deduction reasons, is often communicated separately, trapped in an unstructured email attachment or a scanned PDF remittance advice.

The result: Finance teams spend 30 to 40 per cent of their AR capacity on manual reconciliation activities that deliver no strategic value.

2. Settlement Breaks in the Merchant Model

For organisations operating a merchant facilitation model where customers pay through a payment service provider (PSP) rather than directly to a bank account; this is where the reconciliation challenge is compounded. The gross PSP settlement that appears in a settlement report is almost never equal to the net bank deposit. The difference represents processing fees, FX conversion spreads, rolling reserve movements, and chargeback or refund adjustments.

Each of these components must be identified, classified to the correct GL code, and matched to the originating transaction. Across dozens of PSPs and hundreds of thousands of transactions, this is not a problem that rule-based systems can solve reliably.

3. Manual Load, Audit Risk, and Month-End Pressure

The cumulative effect of the matching gap and settlement breaks is a finance function under chronic manual pressure. Staff time is consumed triaging unidentified cash rather than managing cash flow strategy. Manual adjustments for the workarounds that keep the numbers moving reduce audit traceability. Month-end close stretches to five to seven days due to unresolved reconciliation items. And because the fixes are manual, they do not compound: each month, the process restarts from scratch.

The Agentic Finance Orchestration Framework: Three Pillars

The Agentic Finance Orchestration Framework is built around three functional pillars, each addressing a distinct dimension of the B2B finance challenge. Together, they transform the finance function from a reactive data-processing operation into a proactive, intelligence-led engine.

The architectural principle is consistent across all three pillars: the Agentic AI system sits as an orchestration layer between external data sources and the internal ERP. It does not replace existing systems; it provides the intelligence layer that makes them perform.

Pillar 1: Intelligent Accounts Receivable Automation

The first pillar addresses the core AR challenge: achieving straight-through processing from invoice to cash application, eliminating the manual effort that currently dominates the process.

Continuous Ingestion: The system automatically pulls ERP open items by legal entity on a daily basis and ingests bank statements in MT940 and CAMT.053 format. This creates a live, continuously updated receivables universe with no manual export/import cycles, no end-of-day batch runs, no data that is hours out of date when a collector needs it.

Intelligent Remittance Capture: This is where Agentic AI delivers its most distinctive value. Using a combination of optical character recognition (OCR) and large language model (LLM) extraction, the system reads unstructured remittance advices (whether they arrive as email text, PDF attachments, or portal notifications) and extracts the critical matching fields: invoice IDs, booking references, payment amounts, and currency information. These extracted fields are then paired with the corresponding bank feed entries to enable matching.

Application Logic: The system handles the full spectrum of real-world payment complexity: exact invoice payments, partial payments against a single invoice, short-pays with deduction codes, bulk payments covering multiple invoices, and FX-adjusted receipts where the received amount differs from the invoiced amount due to currency conversion. All application logic is driven by configurable policy rules, ensuring that the system reflects the organisation's actual commercial agreements rather than a generic template.

Pillar 2: Reconciliation of Incoming Payments

The second pillar solves the merchant model challenge: systematically bridging the gap between gross PSP settlements and net bank deposits.

The reconciliation logic works as follows. For each PSP settlement batch, the system ingests the settlement report via API and constructs a detailed waterfall: gross settlement amount, less processing fees (matched to published rate cards), less FX conversion spreads (adjusted for the applicable exchange rate), less rolling reserve movements (tracked on a time-series basis with release scheduling), less chargebacks and refunds (matched to originating transaction records). The resulting figure should equal the net bank deposit. When it does, both sides are automatically classified and posted. When it does not, an exception case is created with all supporting detail pre-populated for human review.

This approach transforms what was a manual investigation process (pulling settlement reports, cross-referencing bank entries, calculating expected fees) into an automated, continuous reconciliation engine that operates at transaction-level granularity.

Pillar 3: Payment Collection Orchestration

The third pillar addresses the outbound side of the cash cycle: turning collections from a reactive, manual chase process into a data-driven, automated orchestration engine.

Partner Segmentation: Before any automation can be effective, the collections strategy must be differentiated. The system segments the partner base by payment risk profile, invoice value, country risk, and historical payment behaviour. High-risk accounts, specially those with a pattern of late payment, disputed invoices, or elevated chargeback rates, are prioritised for direct collector attention. Medium and low-risk accounts are handled through automated workflows.

Automated Dunning Playbooks: For accounts handled automatically, the system executes T-minus logic dunning sequences: a pre-due reminder at T-minus 7 days, an overdue notification at T-plus 1, an SMS alert at T-plus 7, a second email at T-plus 21, and escalation to a human collector at T-plus 30. Each step is configurable by segment, jurisdiction, and invoice value. Templates are personalised with invoice-level detail.

The Human Role Redefined: The most important shift that Agentic AI enables in collections is not the automation of routine tasks; it is the liberation of skilled collectors to focus exclusively on work that requires human judgment. When the AI handles 70 to 80 per cent of routine volume, collectors can spend their time managing complex disputes, building relationships with high-value partners, and negotiating payment plans for accounts at genuine credit risk. This is not headcount reduction; it is a fundamental upgrade in how collection talent is deployed.

The AI Matching Engine: A Tiered Approach to Accuracy and Auditability

One of the most important design principles in enterprise finance AI is that a single confidence model is insufficient. High-value, high-volume financial data demands a matching architecture that can apply appropriate levels of confidence and governance at each tier of complexity.

The Agentic Finance matching engine operates across three tiers:

Tier 1: Deterministic Rules (approximately 60 per cent of transaction volume)

The foundation layer handles cases where the matching evidence is unambiguous: exact match on invoice ID and payment amount, virtual account number matching, known payer combined with exact amount, or ERP reference exact match. These cases are processed automatically with no human review required. The action is straightforward: auto-post to GL.

Tier 2: Heuristic Logic (approximately 25 per cent of transaction volume)

The second tier handles cases where the match is probable but imperfect: small variances attributable to FX conversion or bank fees (handled via configurable tolerance bands), multi-invoice aggregation where a single payment covers several open items, fuzzy matching on payer name or IBAN against known counterparty records, and historical payer pattern recognition. These cases are posted automatically if the heuristic confidence score is within the defined tolerance band; borderline cases are escalated.

Tier 3: AI-Assisted Reasoning (approximately 10 per cent of transaction volume)

The third tier handles genuinely ambiguous cases: unstructured remittance documents where the invoice reference must be inferred from context, partial payment allocations where the AI must reason about the most likely split across multiple open items, and cases where the payer identity is uncertain. The LLM extraction engine produces a confidence score for each proposed match. Cases above the configured confidence threshold are auto-posted; cases below the threshold are routed to the human task inbox with the AI's proposed match, supporting evidence, and confidence score pre-populated.

The Exception Inbox: What Remains for Humans (approximately 5 per cent of volume)

The residual 5 per cent of transactions, those that cannot be resolved even by AI-assisted reasoning, are routed to a structured task inbox. Critically, this is not the same as the manual process it replaces. In a traditional environment, an unidentified payment requires the collector to search ERP records, cross-reference emails, contact the payer, and update multiple systems. In the Agentic AI environment, the exception arrives in the inbox fully researched: candidate matches ranked by probability, supporting documents attached, payer history displayed, and a single-click action to accept the proposed match or override it.

Governance, Security, and Auditability: Enterprise-Grade by Design

Finance automation without governance is not efficiency; it is risk amplification. The Agentic Finance framework is built with enterprise governance requirements as a first-order design constraint, not a retrospective addition.

Human-in-the-Loop Architecture: The system is explicitly designed around the principle that AI handles volume and humans handle judgment. No autonomous action is taken for cases above defined value thresholds without human approval. Write-offs, non-standard allocations, and refunds require explicit approval through a structured workflow. Escalation paths are configurable by role, ensuring that the right person receives the right exception.

Immutable Audit Trail: Every action taken by every agent in the system e.g. every data ingestion, every matching decision, every posting, every exception creation, is logged with a full timestamp and a record of the decision logic applied. The audit trail is immutable: it cannot be modified after the fact. This means that at any point, for any transaction, an auditor can trace the complete journey from raw input data to final GL posting, with the rationale for each step documented.

This is not a minor operational convenience. For organisations subject to SOX 302/404, IFRS 15, or regional financial reporting requirements, the ability to demonstrate full data lineage for every posting is a compliance necessity. Manual processes, by definition, cannot provide this as each adjustment is either undocumented or documented inconsistently.

Financial Controls and Segregation of Duties: The framework enforces segregation of duties through role-based access controls that mirror the organisation's existing approval hierarchy. The same person cannot both initiate a payment allocation and approve a write-off. Dual approval is required for non-standard allocations above defined thresholds. A real-time controls dashboard provides CFOs and finance controllers with a live view of exception volumes, approval queues, and any manual overrides, enabling continuous oversight without manual reporting cycles.

Analytics and Visibility: From Reporting to Conversation

One of the most transformative capabilities that Agentic AI enables is not in the reconciliation engine itself, it is in how finance teams interact with their own data.

"Chat with Data": Natural Language Finance Intelligence

Traditional finance analytics requires a report to be built, scheduled, and distributed before a question can be answered. With natural language query interfaces built on top of the Agentic Finance data layer, any authorised user can ask questions of their receivables data in plain language and receive an immediate, drill-down response.

Examples of queries that can be answered in real time:

"Show me all unapplied cash over €10,000 from last week."

"Which partners in Germany have invoices overdue by more than 60 days?"

"What is our current STP rate by legal entity?"

"Which PSP settlement batches have unresolved breaks from this month?"

This transforms the finance team from consumers of pre-built reports to active interrogators of live data and it changes the speed at which finance leaders can act on emerging issues.

"Chat with Policy": Instant Access to SOPs and Compliance Rules

A complementary capability allows team members to query the organisation's own policy documentation, SOPs, and regional compliance rules in natural language. Rather than searching through shared drives for the relevant write-off policy or calling the regional controller to clarify the correct GL code for a specific fee type, the answer is available instantly.

Predictive Aging and Anomaly Detection

Beyond reactive queries, the analytics layer includes proactive intelligence: AI-driven alerts that flag invoices at risk of aging beyond 60 days based on payer behaviour patterns, anomaly detection that identifies unusual payment patterns or potential duplicate payments before they reach the ledger, and settlement variance analysis that surfaces systematic discrepancies in PSP reporting before they compound.

Six Best Practices for Implementing Agentic AI in Finance

Based on Agentics' experience deploying Agentic AI solutions across global finance functions, the following six principles consistently separate programmes that deliver measurable ROI from those that stall at the pilot stage.

1. Visibility Before Automation

It is not possible to automate what cannot be seen clearly. Every successful Agentic Finance deployment begins with Phase 0: a data discovery and landscape assessment that builds a complete, live view of the receivables universe before a single matching rule is written. Organisations that skip this step i.e. moving directly from business case to automation, consistently encounter data quality surprises that derail the programme.

2. Deterministic First, AI Second

The temptation in AI deployments is to lead with the most sophisticated capabilities. In practice, the most effective deployments lead with high-confidence, deterministic rule-based matching that covers 60 per cent or more of transaction volume before AI reasoning is layered on top for the ambiguous middle. This approach builds trust with finance teams, who are cautious about AI-generated GL postings, and delivers rapid STP improvement that justifies continued investment.

3. Design for the Exception, Not the Rule

The automated path handles itself. The quality of the programme is determined by the quality of the exception workflow i.e. the inbox design, the escalation logic, the approval interface. Organisations that invest in exception workflow design from Day 1 see dramatically higher adoption rates among finance teams and better audit outcomes than those that treat it as a secondary consideration.

4. Governance is an Architecture Decision, Not an Afterthought

Audit trails, segregation of duties, and approval gates must be part of the system architecture from the first line of design. Adding governance controls retrospectively obviously after the matching logic has been built and deployed, is three times more costly, always incomplete, and invariably leaves gaps that create audit exposure. The organisations that achieve SOX-compliant AI-assisted postings are those that treated governance as a Day 1 requirement.

5. One Entity, One Region — Then Scale

The most reliable path to enterprise-scale deployment is the deliberate pilot: a single legal entity, a single payment rail, a defined set of PSP integrations. This approach de-risks the programme, creates a fully tested and documented playbook, and generates the evidence base that drives executive sponsorship for the broader rollout. Programmes that attempt multi-entity, multi-region simultaneous deployment consistently underperform against timeline and budget.

6. Measure What Matters to the CFO

STP rate, DSO reduction, unapplied cash balance, and financial close cycle time are the metrics that earn and maintain executive sponsorship. Before building any capability, map it to a CFO-level metric. If the connection is not clear, the capability is not the right starting point. Every sprint, every phase, every quarterly review should be anchored to movement in these four numbers.

The Business Case: Quantified Value Across Three Dimensions

The commercial case for Agentic AI in finance is not speculative. It is grounded in three measurable value dimensions, each of which can be quantified at the outset of a programme and tracked through deployment.

Dimension 1: Operational Efficiency

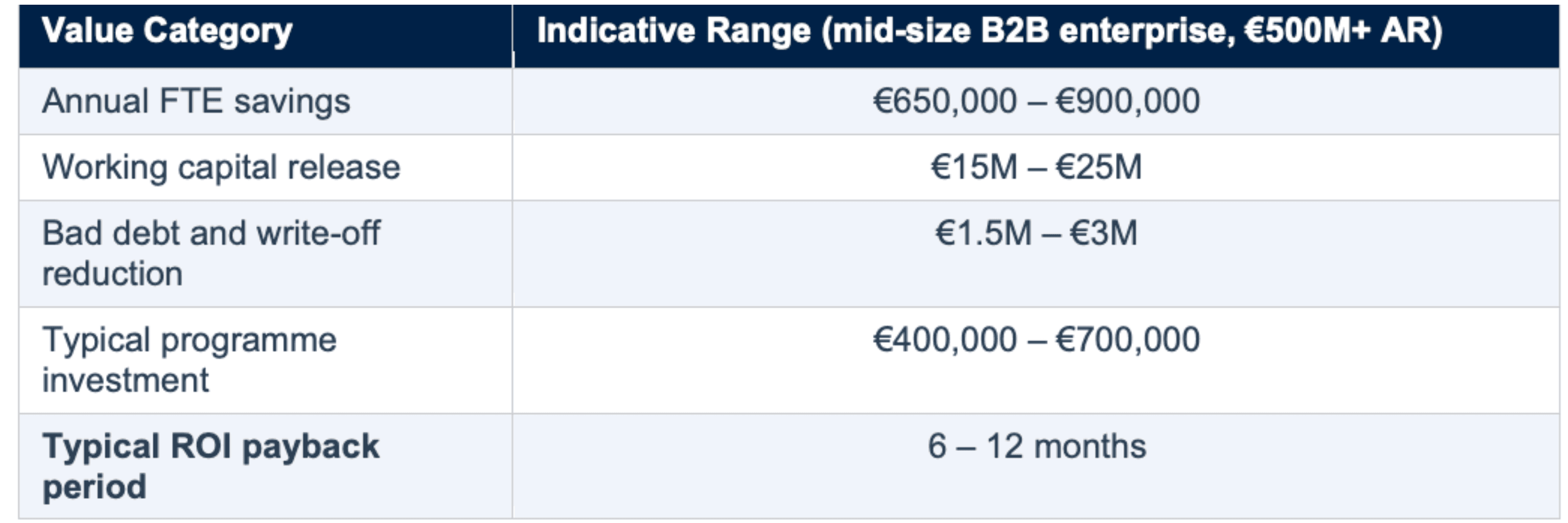

Agentic AR automation typically delivers a 40 to 60 per cent reduction in manual AR effort within the first six months. For a finance team processing significant volumes of B2B receivables, this translates to two to three FTE equivalents redeployed from data processing to value-adding activities such as dispute management, credit risk analysis, and partner relationship management. The FTE cost saving alone without accounting for the quality improvement from removing manual error typically delivers the majority of the programme investment payback.

Dimension 2: Working Capital Impact

Faster cash application and proactive dunning reduce days sales outstanding (DSO) by eight to twelve days within six months of deployment. For a business with €1 billion in annual revenue, each DSO day freed represents approximately €2.7 million in working capital released. A 10-day DSO improvement therefore generates €27 million in working capital impact; dwarfing the typical programme investment by an order of magnitude.

Dimension 3: Risk and Compliance Value

The compliance value of the programme is harder to quantify but arguably the most durable. Full audit traceability for every posting eliminates the manual documentation burden at period-end. Month-end close accelerates by two to three days. Audit preparation time reduces by 60 to 70 per cent. And the risk of a material misstatement due to unidentified cash or unreconciled settlement breaks, a genuine exposure for large organisations operating at hybrid-model scale, is systematically reduced.

The Phased Implementation Roadmap

The deployment philosophy for Agentic Finance is consistent with the best practice principle above: visibility first, then automation. Each phase is designed to deliver standalone value, ensuring that the programme generates return at every stage rather than requiring full deployment before any benefit is realised.

Phase - Scope and Deliverables |

PHASE 0: Blueprint (2–4 weeks) Data discovery and landscape assessment. ERP and PSP connectivity analysis. Write-off threshold and FX tolerance policy definition. Pilot entity and region selection. |

PHASE 1: Foundation (4–6 weeks) Data ingestion pipeline deployment. Live AR visibility dashboard. Bank statement feed integration. PSP settlement API connection. |

PHASE 2: Cash App: AR (6–8 weeks) Tier 1 deterministic matching go-live. Remittance AI extraction deployment. Auto-posting of high-confidence matches. Exception task inbox operational. |

PHASE 3: Settlement Recon (4–6 weeks) PSP gross-to-net reconciliation engine. Fee and reserve automated classification. FX tolerance matching logic. Daily break reporting. |

PHASE 4: Collections (4–6 weeks) Partner risk segmentation model. Automated dunning playbook engine. T-minus logic sequence deployment. Full analytics dashboard. |

Conclusion: The Finance Transformation Imperative

The finance department that waits for a perfect AI strategy will be outpaced by one that starts with a 10-week pilot. The technology for Agentic Finance is not emerging, it is proven. The data formats are known. The integration patterns are established. The governance frameworks are available. The only variable is organisational readiness and the decision to begin.

The question for finance leaders is no longer whether Agentic AI will transform B2B finance operations. That transformation is already underway. The question is whether your organisation leads it by building the capability, the institutional knowledge, and the competitive advantage that comes from early deployment or reacts to it, scrambling to match the operational efficiency of peers who moved first.

The Agentic Finance Orchestration Framework offers a de-risked, value-first path to that transformation: visibility before automation, deterministic logic before AI reasoning, pilot before scale, governance from Day 1. It is not a big-bang transformation programme. It is a systematic capability build that delivers measurable ROI at every phase gate, with each milestone creating the foundation for the next.

For finance leaders who are ready to move from evaluation to action, the starting point is a 90-minute Discovery Session: validate scope, map the PSP landscape, and identify the Pilot Slice that can prove value in under 10 weeks.

About Agentics

Agentics is a boutique AI transformation firm that builds, scales, and optimises Agentic AI solutions for enterprise clients across financial services, healthcare, manufacturing, and professional services. We are a coalition of strategists, growth architects, and AI engineers who combine board-level strategic perspective with ground-level engineering execution, drawn from large-scale transformations at the world's leading IT, consulting, and AI firms delivered without the overhead of big-consultancy engagements.

Our proprietary Validation-First Framework with De-Risk Disruption methodology ensures that every engagement delivers measurable ROI, de-risked deployment, and full organisational adoption not just a technology implementation.

This article is the third in the Agentics Thought Leadership Series on AI Transformation. Volume I covers Agentic AI in Marine Insurance. Volume II covers Agentic AI in Pharmaceutical Generics.

© 2026 Agentics. All content in this article is the intellectual property of Agentics and is published for informational purposes. Statistics cited from McKinsey Global Institute, IOFM, and Ardent Partners B2B Payments 2024.

Related Post