The Enterprise Agentic AI Landscape 2026

Enterprise AI in 2026 is no longer a question of whether organisations adopt agents. It is a question of whether they can make agents safe, measurable and business-relevant at scale. Across the leading global surveys, the pattern is identical: Adoption has outrun Readiness. Enterprises have deployed generative AI broadly for everyday work, but far fewer have built the governance, data quality and process context required to let agents act autonomously inside real business processes. That gap, NOT Model Capability is the defining story of the market this year.

Posted by

The Agentics

Posted at

Enterprise AI

Posted on

DIFFERENT LENSES, ONE CONCLUSION: Ambition is near-universal; governed, value-generating execution is the exception.

THE SHORT ANSWER

Enterprise AI in 2026 is no longer a question of whether organisations adopt agents. It is a question of whether they can make agents safe, measurable and business-relevant at scale.

Across the leading global surveys, the pattern is identical:

Adoption has outrun Readiness.

Enterprises have deployed generative AI broadly for everyday work, but far fewer have built the governance, data quality and process context required to let agents act autonomously inside real business processes.

That gap, NOT Model Capability is the defining story of the market this year.

The Headline Tension

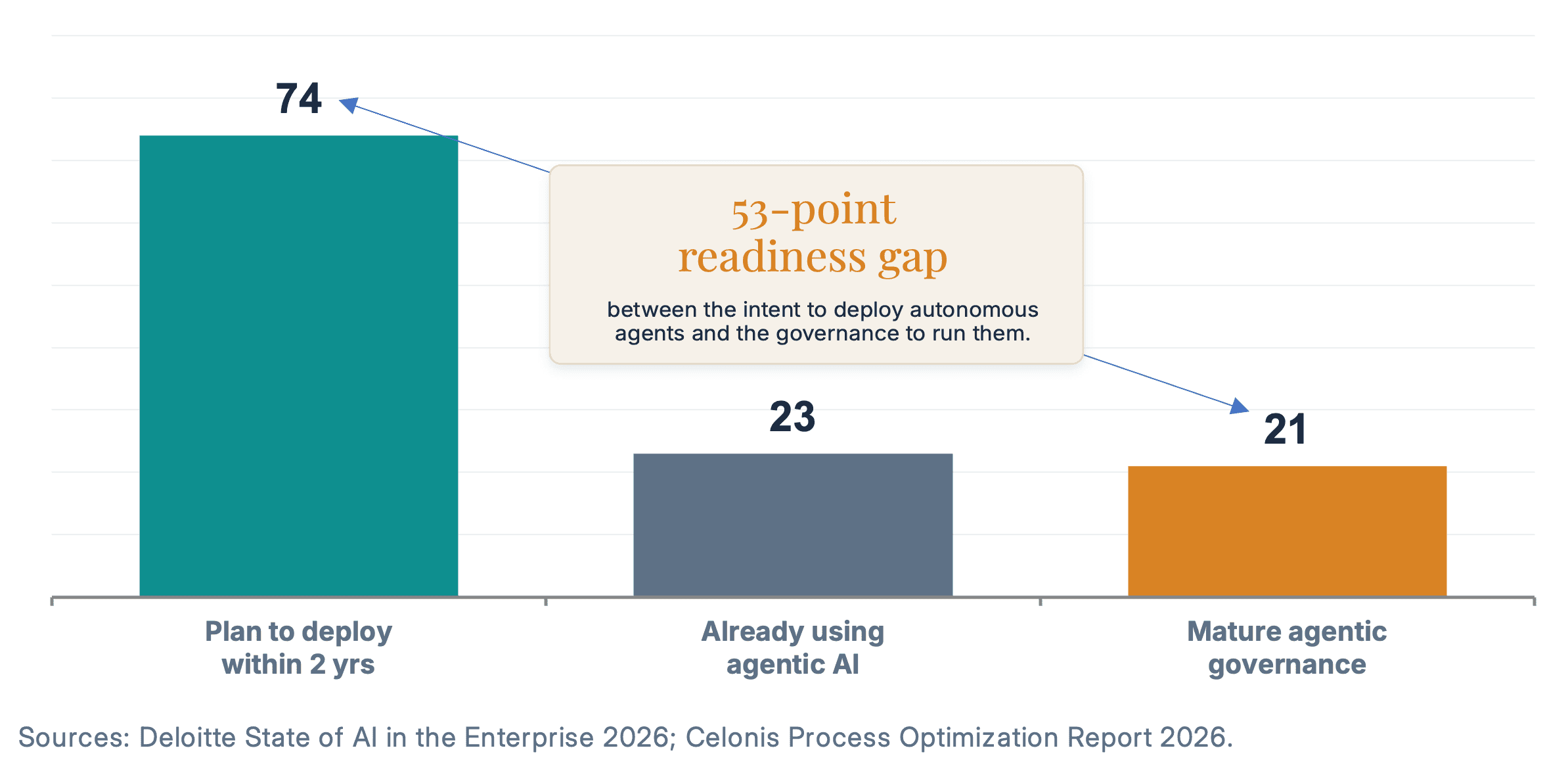

→ Deloitte’s 2026 survey of 3,235 leaders across 24 countries finds that roughly three-quarters of enterprises expect to use agentic AI at least moderately within two years, yet only 21% have a mature governance model for autonomous agents.

→ Celonis, surveying 1,649 senior leaders, finds 85% aspire to become an “agentic enterprise” within two-to-three years, while 60% say they still cannot adapt operations fast enough to realise ROI.

→ And MIT’s widely cited 2025 study reports that 95% of generative-AI pilots delivered no measurable profit-and-loss impact.

What Leaders Should Take Away

• Adoption is broad, integration is shallow. Most enterprises have approved tools and live use cases; far fewer have redesigned roles, processes and oversight around AI.

• The bottleneck is execution architecture, not the model. Fragmented systems, weak process-data quality, missing business context and IT–business misalignment are what stall scale.

• Governance is the catalyst, not the brake. Enterprises where senior leadership actively shapes AI governance capture materially more value than those that delegate it to technical teams alone.

• Value, not productivity, is the new bar. The market is moving from “Can it do the task?” to “Can it improve the business?” and budgets increasingly follow measurable P&L outcomes.

• The winners scale deliberately. They start with lower risk use cases, build governance first, validate on real data, and expand in stages rather than chasing autonomy for its own sake.

“Most enterprises are not failing because of weak AI models. They are failing because they are trying to scale intelligence without building the governed execution layer that makes intelligence usable in the real world.” — Nishith Srivastava (Nish), Founder, The Agentics Co.

The 2026 Market State

The 2026 landscape is defined by momentum colliding with friction. On one axis, intent has never been higher. Deloitte reports that workforce access to sanctioned AI tools has expanded by roughly 50% in a single year, and that 85% of companies expect to customise agents to their own business needs.

On the other axis, the foundations needed to operationalise that intent are uneven and in several dimensions, leaders feel less prepared than a year ago on infrastructure, data, risk and talent.

Adoption is High; Governance is NOT Keeping Pace

Deloitte frames the gap precisely: by 2027, 74% of respondents expect to use AI agents at least moderately, 23% extensively, and 5% as a core component of operations. Yet about 80% of organisations currently lack the governance capabilities agentic AI requires clear boundaries on which decisions an agent may take independently, real-time monitoring that flags anomalies, and audit trails that capture the full chain of agent actions.

The risks leaders worry about most are themselves governance risks: data privacy and security (73%), legal/IP/regulatory compliance (50%), oversight capability (46%) and model explainability (46%).

A useful external check on value realisation

MIT’s GenAI Divide: State of AI in Business 2025 analysed 300+ deployments and reported that 95% of generative-AI pilots produced no measurable P&L impact, with the few successes concentrated in deeply integrated, domain-specific, often vendor-delivered systems. The figure has been debated, critics note its six-month P&L definition ignores efficiency and CX gains, but even sceptics accept the underlying signal: High Adoption, Low Transformation. It is the same divide Deloitte and Celonis describe from the inside.

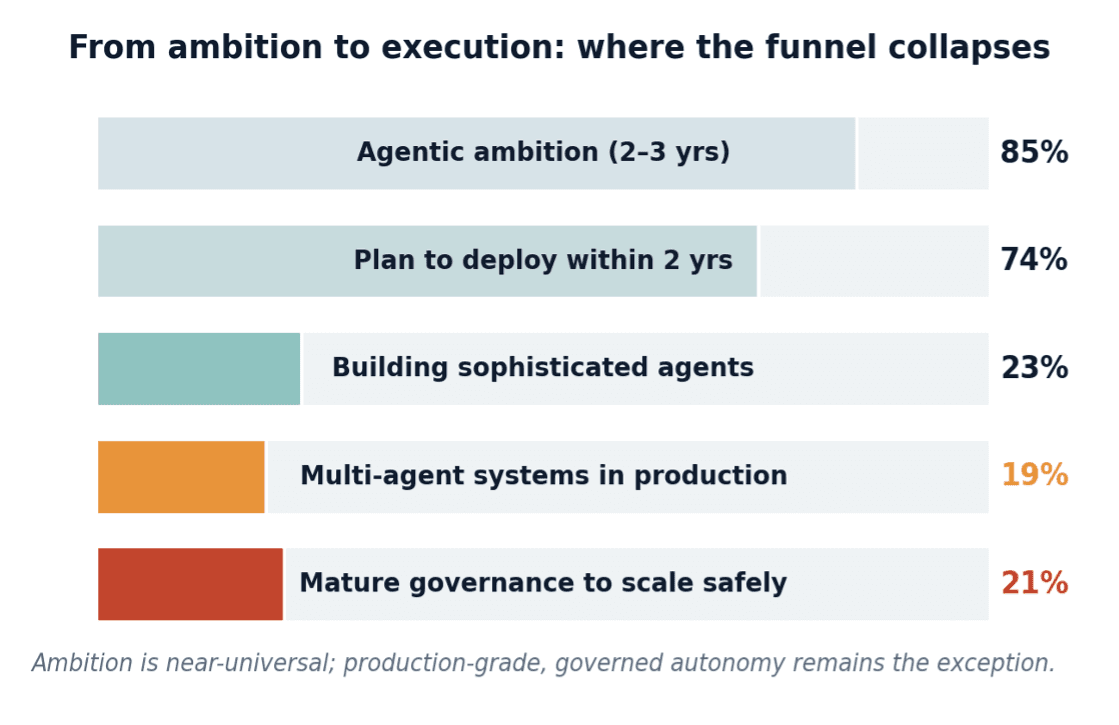

Agentic Ambition vs Operational Readiness

Celonis quantifies the operational side of the same problem. 85% of businesses aim to become an agentic enterprise within two-to-three years, but 76% admit they are only “getting by” with sub-optimal processes, 67% have concerns about the data they would feed those processes, and 60% cannot adapt operations quickly enough to capture ROI.

Crucially, 82% of leaders agree AI can only deliver ROI if it understands how the business actually runs yet 45% struggle to give AI that business context (rules, KPIs, enterprise architecture).

Figure 2: The ambition-to-execution funnel. Near-universal intent narrows sharply at production-grade, governed autonomy.

Sources: Celonis 2026; Deloitte 2026.

3. What Enterprises Are Actually Doing

Strip away the narrative and enterprise AI adoption splits cleanly into two layers.

→ The first layer is broad productivity: copilots, content generation, workflow assistance and internal Q&A.

→ The second layer is true agency: systems that plan, take actions, coordinate across tools and adapt inside business processes.

The first is widespread; the second remains constrained by governance, integration and process maturity.

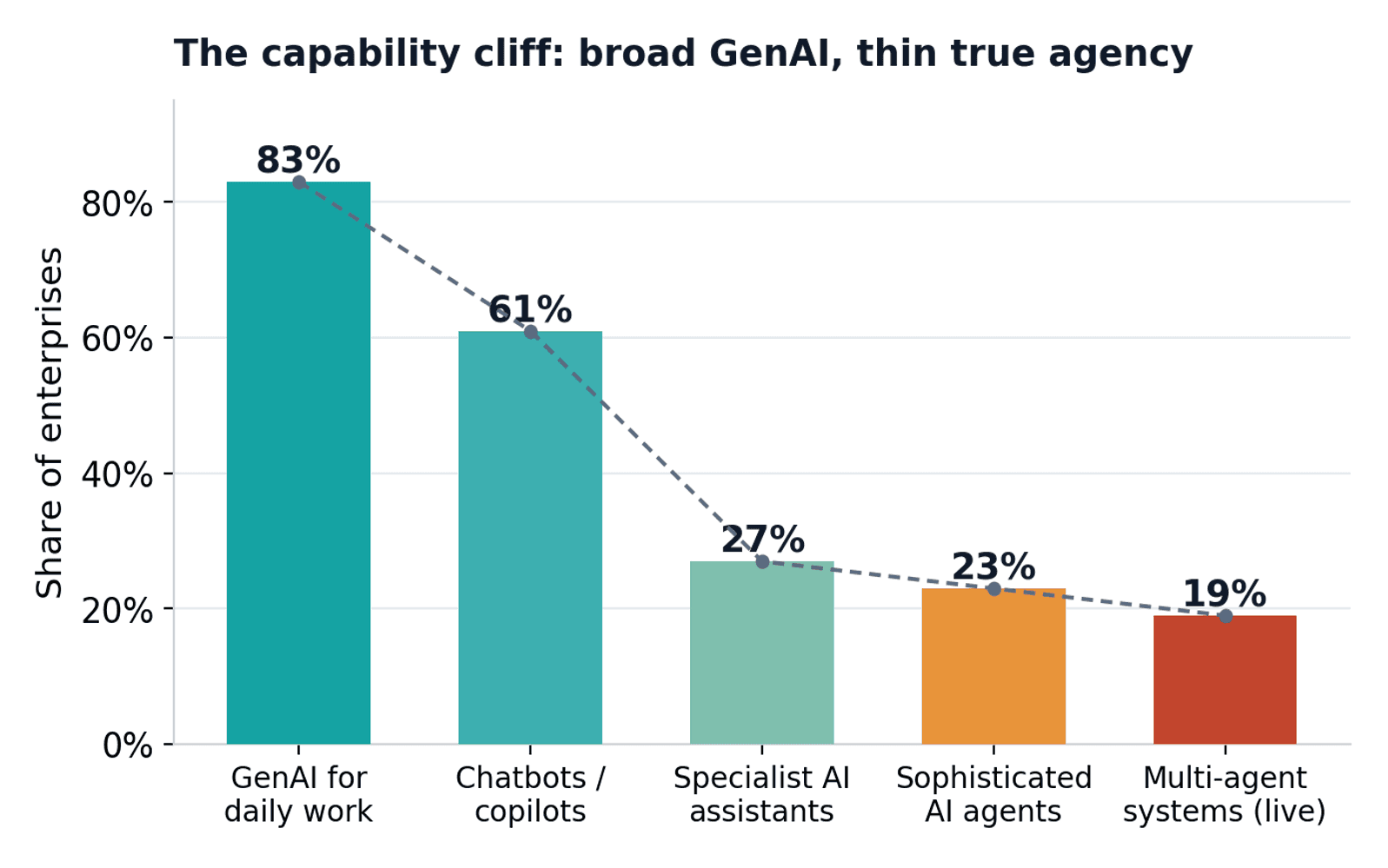

Figure 3: The capability cliff. Adoption falls away sharply as sophistication rises.

Source: Celonis Process Optimization Report 2026 (1,649 leaders).

The descent is stark.

While 83% use GenAI for daily work and 61% deploy chatbots or copilots, only 27% are building specialist AI assistants and 23% are developing sophisticated agents. The encouraging signal sits at the far edge: 19% of enterprises already run multi-agent systems and a further 71% are exploring them; a fast transition from single-point automation toward orchestrated AI work systems is clearly underway, even if production remains early.

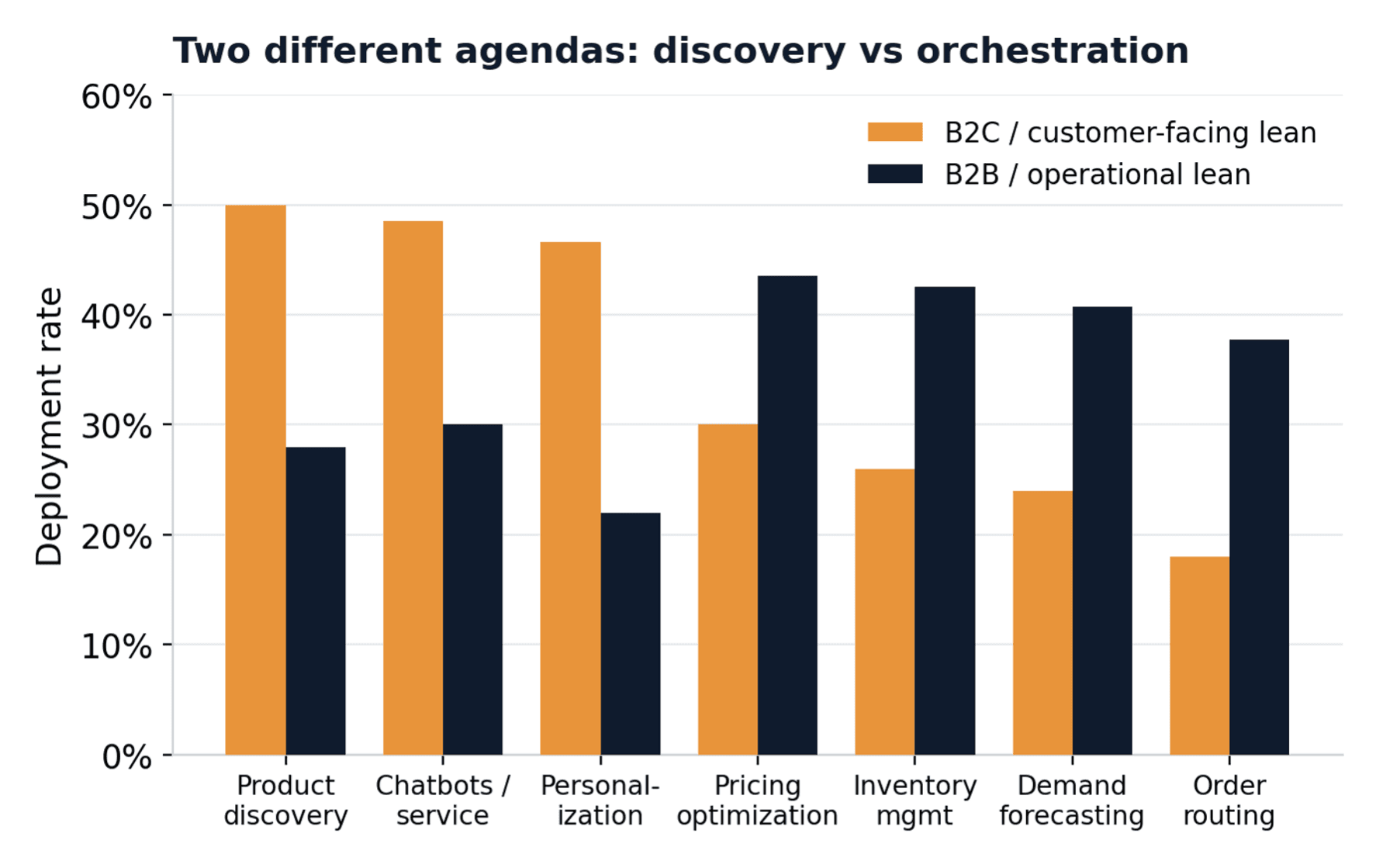

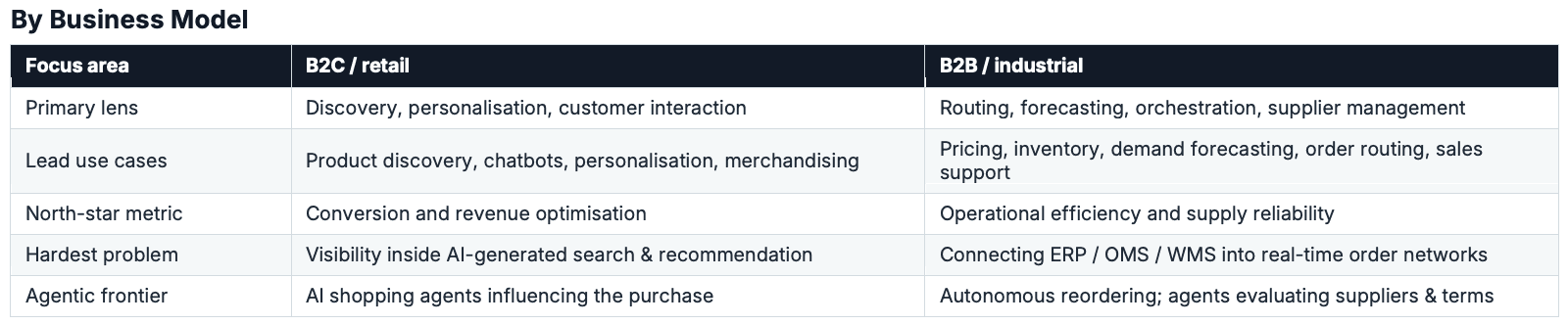

The B2B / B2C Divergence in Commerce

Commerce data shows how this plays out across segments. A 2026 study of 600 ecommerce decision-makers (Logicbroker / Midsail Research) found that 95.5% have deployed at least one AI capability, but the entry points differ by model.

B2C and retail brands lean toward customer-facing intelligence i.e.

→ Product discovery (~50%),

→ Chatbots (48.5%) and

→ Personalisation (46.6%).

B2B organisations push harder into operational orchestration i.e.

→ Pricing optimisation (43.5%),

→ Inventory management (42.5%),

→ Demand forecasting (40.7%) and

→ Order routing (37.7%)

Figure 4: Two different agendas. B2C optimises discovery and interaction; B2B optimises orchestration and supply. Source: Digital Commerce 360 / Logicbroker 2026.

Where the money is going

Nearly half of surveyed commerce organisations (47.3%) plan to invest at least $1M in AI commerce initiatives over the next 12 months, and 7.3% expect to spend more than $10M.

The objectives are unambiguously commercial:

→ Revenue Growth (50.2%),

→ Customer experience (46%),

→ Cost reduction (45.5%) and

→ Operational efficiency (44.5%).

Only 12% cite a lack of executive support as a barrier, the obstacles are technical:

→ Security and privacy (42.5%),

→ Data quality (40.2%) and

→ Integration complexity (36.3%).

Why Most Programmes Stall

This is the analytical heart of the paper, and its thesis is blunt: the enterprise is not failing at model capability. It is failing at execution architecture. The blockers that surface across Deloitte, Celonis and MIT are remarkably consistent, and almost none of them are about the intelligence of the model itself.

Figure 5: Readiness blockers ranked by frequency. Every leading blocker is organisational or architectural, not a model limitation. Sources: Deloitte 2026; Celonis 2026.

The Five Recurring Failure Modes

Weak governance. Only ~21% have mature agentic governance. Without decision boundaries, real-time monitoring and audit trails, autonomy becomes liability. Agents can make unseen mistakes, work at cross-purposes or expose sensitive data, and those risks compound when pilots scale.

Fragmented systems and poor data quality. Complex, outdated or disconnected systems (45%) and poor process-data visibility (43%) top the operational blocker list. MIT, Gartner and RAND independently trace most stalled programmes to data readiness rather than the model.

Missing business context. 82% of leaders say AI only delivers ROI if it understands how the business runs; 45% cannot supply that context. An agent without rules, KPIs and process awareness produces output that is fast but not trustworthy.

IT–business misalignment. 45% cite misalignment between IT and business stakeholders, and 47% a shortage of internal AI expertise. The capability gap is human and organisational before it is technical.

No role or operating-model redesign. 84% of companies have not redesigned jobs around AI capabilities. Bolting agents onto an unchanged operating model caps the upside at incremental productivity and forecloses genuine transformation.

The Execution-Architecture Argument, in One Line

The organisations reporting AI-driven P&L gains in 2026 are not the ones with better models. They are the ones that stopped running new pilots and fixed their data, process and governance foundations first then layered intelligence on top of operations it could actually understand.

“Too often, enterprises buy plug-and-play tools expecting instant results, bolt AI onto outdated systems with no long-term strategy, or run scattered pilots that never scale. The result is wasted time, wasted budgets, and zero ROI. The antidote is AI-native transformation to prove value on the client’s own data first, then scale in modular stages tied to measurable outcomes.” — Nishith Srivastava (Nish), Founder & CEO, The Agentics Co.

Adoption Patterns by Segment

Adoption is not monolithic. It varies by company size and by business model. The matrices below summarise where each segment concentrates its effort and where its characteristic risk lies.

A telling convergence: in the 2026 commerce study, hybrid organisations serving both B2B and B2C were the single largest group (44.8%), reflecting how quickly the two playbooks are merging as agents move from the storefront into the supply chain. The strategic implication is that the orchestration layer is where durable advantage now accrues.

6. Cases and Signals from the field

Rather than over-claim named case studies, we combine verifiable named signals with research-grounded patterns. Each illustrates one facet of the adoption-to-value gap.

Named Investment Signals

• Bosch announced plans to invest more than $2.9B in AI, underlining how industrial leaders are treating AI as core infrastructure rather than experiment. (Digital Commerce 360, Jan 2026)

• Genuine Parts and Avnet deepened digital, data and AI investment through late-2025/early-2026 earnings, a B2B distribution pattern of embedding AI into pricing, forecasting and fulfilment. (Digital Commerce 360)

• Amazon and Walmart are pursuing visibly different agentic-commerce strategies, a reminder that even the most advanced players are still defining how autonomous purchasing should work. (Digital Commerce 360, Mar 2026)

Pattern-based Examples

COMMERCE: Broad deployment, uneven depth (Digital Commerce 360 / Logicbroker)

95.5% of surveyed commerce enterprises have deployed at least one AI capability, and 90.7% believe AI will influence at least 20% of orders by 2027 yet the binding constraint is connecting CRM, OMS, WMS, ecommerce and PIM systems into real-time order networks. Breadth is easy; orchestration is the moat.OPERATIONS: Context is the differentiator (Celonis)

Enterprises that treat process intelligence as the foundation, making how the business actually runs legible to AI, are the ones positioned to convert agentic ambition into ROI. Those that skip it inherit the 60% “can’t adapt fast enough” problem.GOVERNANCE: Scaling faster than guardrails (Deloitte)

With ~80% of organisations lacking mature agentic governance, Deloitte’s explicit warning is that retrofitting oversight after deployment is slower and costlier than designing it in. The most successful firms start with lower-risk use cases and build governance capability before they scale.

The Agentics - Point of View

Our reading of the 2026 evidence is consistent with a position we have held since founding: the move that matters is from rule-based automation to reasoning engines, orchestrated as multi-agent systems and crucially, governed at the action layer. AI-native is not a tagline; it is an operating system.

Three principles follow.

Validation-first, NOT Pilot-First

Prove value on the client’s own data before scaling.

A staged model — proof of concept → pilot on real data → phased rollout → optimisation, is what prevents the cascading failures that produce the 95% pilot-stall statistic. Every stage is tied to a KPI: revenue growth, cost reduction or productivity.Governed Execution as the Enabling Layer

Autonomy without governance is liability. Decision boundaries, real-time monitoring, audit trails and human escalation paths are not compliance overhead bolted on afterwards, they are part of operational design, and they are what makes scaling possible at all. This is the “governed execution layer” we believe most enterprises are missing.Orchestration over Single Agents

The frontier is not one better chatbot; it is many specialised agents working in concert, a conductor coordinating systems toward a shared business outcome. The 19%-live / 71%-exploring split on multi-agent systems is, in our view, the leading indicator of where durable advantage will form over the next 24 months.

What leaders should do in the next two quarters

Fix the foundation first: Audit data and process readiness before launching new pilots.

Govern before you scale: Stand up decision boundaries, monitoring and audit trails now.

Pick provable use cases: Lower-risk, high-volume, measurable.

Redesign the work: Change roles and operating models, don’t just add tools.

Measure business outcomes: Hold every deployment to a P&L or efficiency KPI, not a demo.

Methodology & Sources

This paper synthesises publicly available research published between mid-2025 and mid-2026. It does not contain original survey data; every statistic is attributed to its primary source below. Where a figure is contested (notably the MIT 95% pilot-failure number), we have noted the debate rather than presenting it as settled fact. Figures in charts are drawn directly from the cited surveys; the B2B/B2C emphasis chart uses representative deployment rates from the Digital Commerce 360 / Logicbroker study to illustrate directional differences, not segment-exclusive splits.

Primary Sources

• Deloitte — State of AI in the Enterprise 2026 (“The Untapped Edge”), 3,235 leaders, 24 countries, Aug–Sep 2025. https://www.deloitte.com/us/en/about/press-room/state-of-ai-report-2026.html

• Deloitte Insights — “Agentic AI is scaling faster than guardrails,” Apr 2026. https://www.deloitte.com/us/en/insights/topics/emerging-technologies/ai-agents-scaling-faster.html

• Celonis — 2026 Process Optimization Report (“The Year the Agentic Enterprise Takes Flight”), 1,649 leaders. https://www.celonis.com/blog/2026-the-year-the-agentic-enterprise-takes-flight

• Digital Commerce 360 — “B2B and B2C companies increase AI investment as agentic commerce gains traction,” Mar 2026 (Logicbroker / Midsail Research, 600 decision-makers). https://www.digitalcommerce360.com/2026/03/13/b2b-b2c-ai-investment-agentic-commerce-traction/

• MIT NANDA — The GenAI Divide: State of AI in Business 2025 (300+ deployments). https://fortune.com/2025/08/18/mit-report-95-percent-generative-ai-pilots-at-companies-failing-cfo/

• The Agentics Co. — Company positioning and Validation-First framework. https://theagentics.co/

© 2026 The Agentics Co. Enterprise AI transformation, specialising in Agentic AI and Multi-Agent Systems.

Amsterdam · Europe · Middle East · APAC · LATAM.

https://TheAgentics.co

Free to cite with attribution to The Agentics Co., 2026.

Related Post